Ransomware is malware that encrypts an individual's files so that they no longer have access to them, and subsequently demand payment for the files to be released. Usually the payment is asked to be made in an untraceable cryptocurrency form, such as Bitcoin. The most common way ransomware ends up on an individual's computers is through email spam, which individuals will click on and open.

Unfortunately, the files cannot be decrypted without a mathematical key which is only known by the cyber attacker, and the reason why many individuals tend to pay up. However, many find that despite paying the ransom, their files remain encrypted.

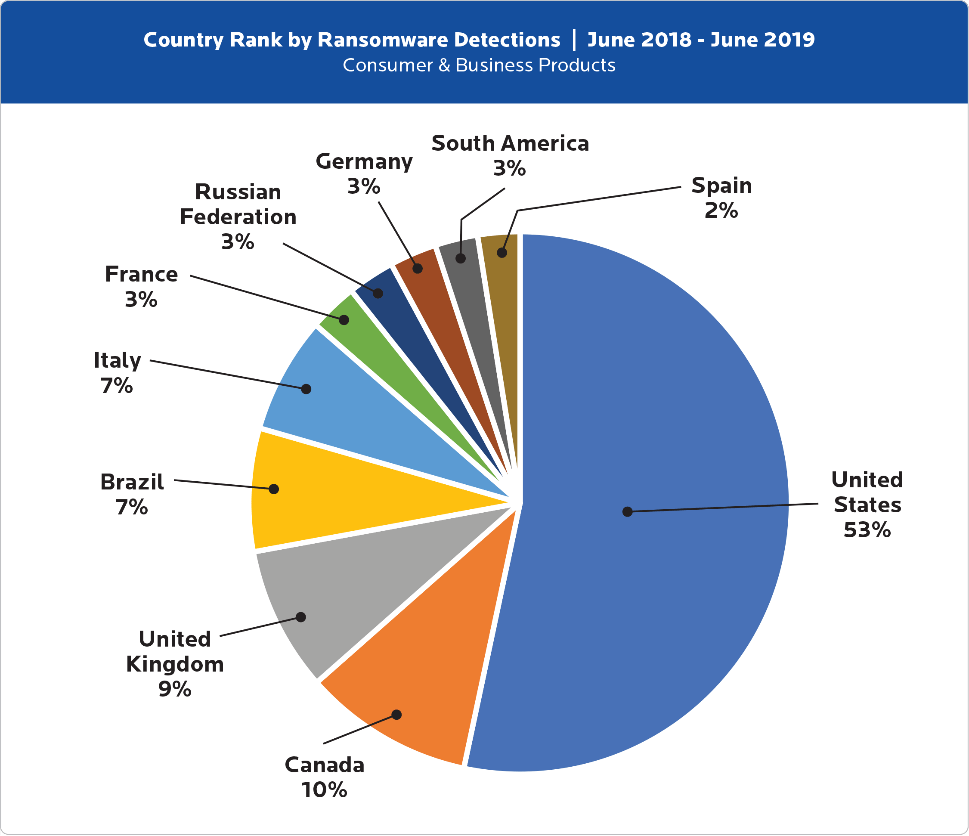

When looking at which countries were affected by ransomware attacks the most, the UK was found to have the highest percentage out of Europe:

Figure 1: Cybercrime Tactics and Techniques: Ransomware Retrospective Report, Malwarebytes

Despite the NHS facing one of the worst ransomware attacks in May 2017 - the WannaCry ransomware attack - which cost the NHS £92m and caused more than 19,000 appointments to be cancelled (The Department of Health), this chart clearly highlights how organisations in the UK still need to invest more into their Cyber Security solutions to stay protected from ransomware attacks.

At Exponential-e, we help organisations that have been affected by ransomware attacks. Our Head of Cyber Consultancy, Mark Belgrove, discusses a real-life cyber attack in the video below, and shares how Exponential-ehelped mediate the situation.